HELOC Calculator – Calculate Your Home Equity Line of Credit Payment

| HELOC Amount | — |

| Interest Rate | — |

| Draw Period | — |

| Repayment Period | — |

| Total Payments | — |

| Payoff Date | — |

| Interest (Draw Phase) | — |

| Interest (Repayment Phase) | — |

| Total Interest Paid | — |

| Total Amount Paid | — |

| Date | # | Payment | Interest | Principal | Balance |

|---|

If you own a home and need cash — for a renovation, debt payoff, or a large expense — a HELOC is one of the most cost-effective ways to borrow. But before you call a lender, you need to know what the payments actually look like.

Use the HELOC calculator above to get your exact monthly payment, full amortization schedule, and a side-by-side view of your draw period vs. repayment period costs.

What Is a HELOC?

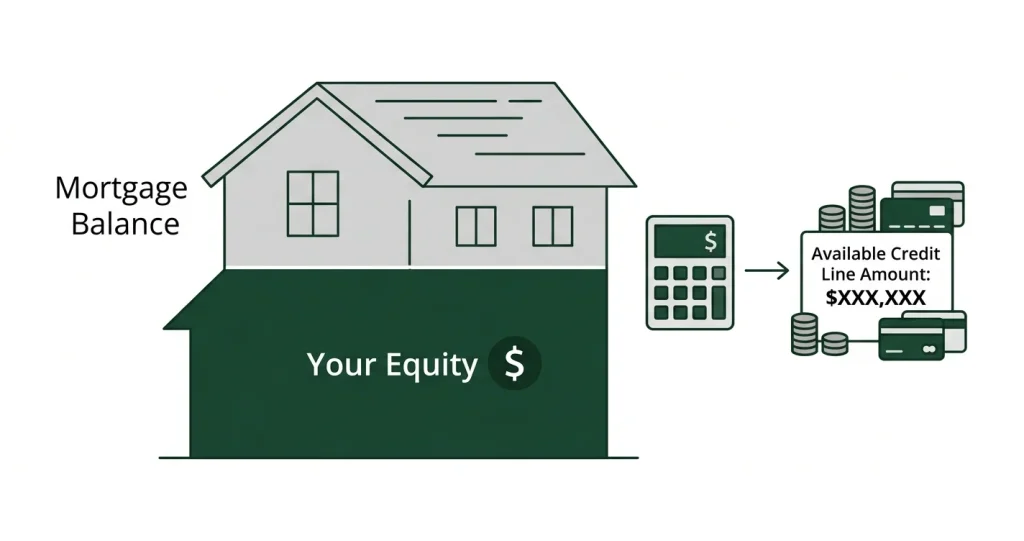

A home equity line of credit (HELOC) lets you borrow against the equity in your home — the difference between what your home is worth and what you still owe on your mortgage.

Think of it like a credit card secured by your house. You get a credit limit, you borrow what you need, repay it, and borrow again — all during a set “draw period.” Unlike a home equity loan, you don’t receive a lump sum upfront. You draw funds as you need them.

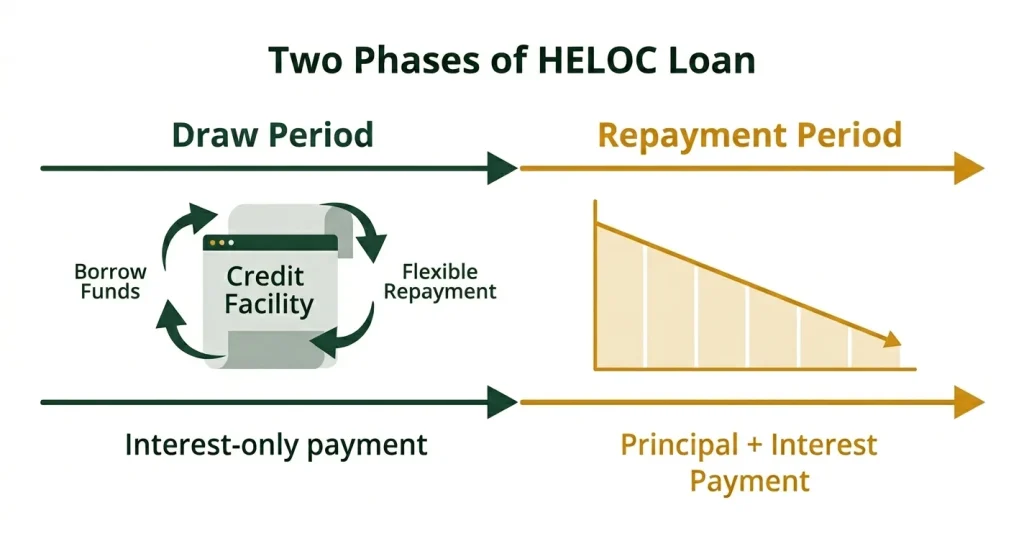

HELOCs typically come in two phases:

Draw period — usually 5 to 10 years. You can borrow and repay freely. Most lenders only require interest payments during this time, which keeps your monthly payment low.

Repayment period — usually 10 to 20 years. The credit line closes. You repay the remaining balance in fixed principal-plus-interest payments. Your monthly payment increases, sometimes significantly.

This two-phase structure is what makes HELOCs different from other home loans — and it’s exactly what the calculator above accounts for.

How the HELOC Calculator Works

The calculator runs two separate calculations: one for your draw period and one for your repayment period.

Draw Period Payment

During the draw period, your minimum monthly payment is interest-only:

Monthly Payment = HELOC Balance × (Annual Rate ÷ 12)

For example: a $100,000 HELOC at 8.75% has a monthly draw payment of $729.17.

If you choose to pay principal during the draw period, the calculator switches to the full amortization formula — the same one used for mortgage payments — so you see exactly how much faster you’d pay down the balance.

Repayment Period Payment

Once the draw period ends, the remaining balance gets amortized over the repayment term:

Monthly Payment = Balance × [r(1+r)^n] ÷ [(1+r)^n − 1]

Where r = monthly rate, n = number of repayment months.

Using the same $100,000 example at 8.75% with a 20-year repayment: your monthly payment jumps to $884. That’s the “payment shock” many homeowners aren’t prepared for. The calculator shows you this number before you commit to anything.

LTV Check

The calculator also computes your combined loan-to-value ratio (CLTV):

CLTV = (Mortgage Balance + HELOC Amount) ÷ Home Value × 100

Most lenders cap CLTV at 80–85%. If your inputs push past that limit, the calculator flags it and tells you the maximum HELOC amount you actually qualify for.

HELOC Rates in 2026

HELOCs are variable-rate loans. Your rate is tied to the prime rate, which moves with Federal Reserve decisions.

As of 2026, the prime rate sits around 7.5%. Most lenders price HELOCs at prime plus a margin of 0.5–2%, putting typical rates between 8.0% and 9.5% for well-qualified borrowers. Borrowers with lower credit scores or higher CLTV ratios can see rates of 10–12%.

A few lenders now offer rate-lock options on a portion of your HELOC balance, converting it to a fixed rate. This costs slightly more but protects you if rates rise.

The calculator includes a rate scenario tool. Run your numbers at your current rate, then again at +1% and +2% to see how a rate increase would affect your monthly payment. It takes 10 seconds and can save you from a nasty surprise later.

What Affects Your HELOC Rate?

How Much HELOC Can I Get?

Your maximum HELOC depends on three numbers: your home value, your mortgage balance, and the lender’s maximum CLTV.

Maximum HELOC = (Home Value × LTV Limit) − Mortgage Balance

Example:

Maximum HELOC = ($500,000 × 0.80) − $280,000 = $400,000 − $280,000 = $120,000

At 85% LTV: ($500,000 × 0.85) − $280,000 = $425,000 − $280,000 = $145,000

The higher the LTV limit your lender allows, the larger your available credit line — but your rate will likely be higher too.

Enter your numbers into the calculator above and it does this math instantly, including a flag if your requested HELOC amount exceeds what your equity supports.

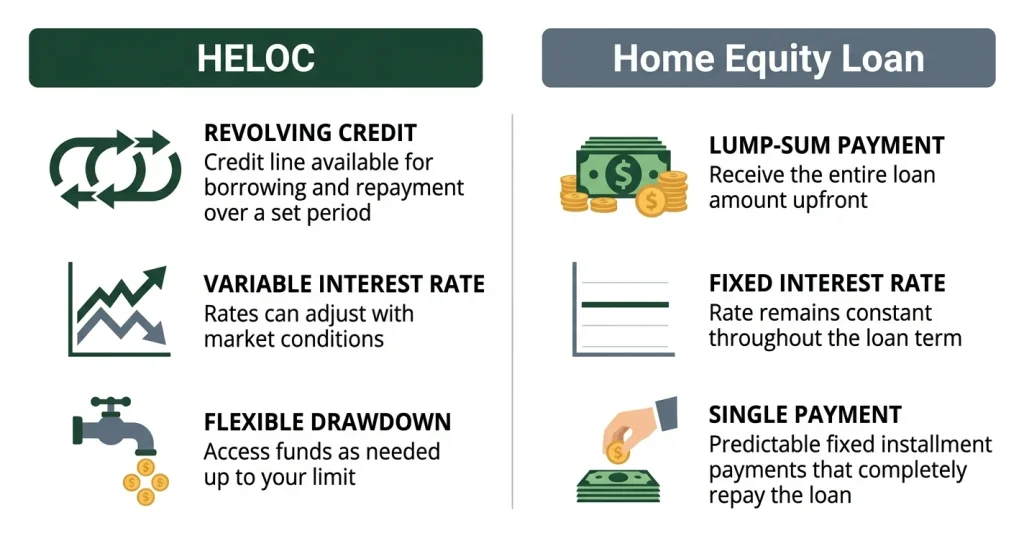

HELOC vs. Home Equity Loan: What’s the Difference?

Both products let you borrow against home equity. The difference is in structure.

HELOC | Home Equity Loan | |

|---|---|---|

How you receive funds | Draw as needed | Lump sum upfront |

Interest rate | Variable (usually) | Fixed |

Monthly payment | Varies during draw | Fixed from day one |

Best for | Ongoing projects, flexible needs | One-time large expense |

Risk | Payment shock at repayment | Rate locked, more predictable |

A HELOC works well for home renovations where costs are uncertain or spread over time. A home equity loan is better when you know the exact amount you need and want payment certainty.

Neither is universally better. It depends on your situation.

HELOC Draw Period vs. Repayment Period

This is the part most borrowers underestimate.

During a 10-year draw period on a $100,000 HELOC at 8.75%, you pay $729/month — interest only. Total paid: $87,480. Your balance is still $100,000.

Then repayment starts. Over 20 years at the same rate, you pay $884/month. That’s a $155 jump. And over the full repayment period, you pay another $112,160 in interest.

Total cost of borrowing $100,000: $199,640.

That’s not a knock on HELOCs — for the right use case, they’re still cheaper than alternatives. But you should know this number before you borrow.

The amortization schedule in the calculator shows every payment, every month, for the full loan term. You can see exactly when the balance starts dropping and how much interest you’re paying at each stage.

What Happens at the End of the Draw Period?

The draw period ends and the repayment period begins. You can no longer borrow from the line of credit. Your minimum payment increases because you’re now paying principal.

Some lenders allow you to renew or extend the HELOC at the end of the draw period, but this isn’t guaranteed. Plan for the higher repayment payment from day one.

Interest-Only vs. Principal + Interest During the Draw Period

Most borrowers make interest-only payments during the draw period because that’s the minimum required. But paying principal during this phase has real advantages.

If you pay an extra $200/month toward principal on a $100,000 HELOC during the draw period, you reduce the balance before repayment starts — which lowers both the repayment payment and the total interest you’ll pay.

The calculator lets you switch between interest-only and principal-plus-interest draw payments so you can see the difference side by side.

Is HELOC Interest Tax Deductible?

It depends on how you use the money.

Under current IRS rules (Publication 936), HELOC interest is deductible only if the funds are used to buy, build, or substantially improve the home that secures the loan. Using a HELOC to renovate your kitchen qualifies. Using it to pay off credit cards or fund a vacation does not.

If you itemize deductions and use the HELOC for home improvements, the interest deduction can reduce your after-tax cost of borrowing — which makes the effective rate cheaper than the stated rate.

Talk to a tax professional before assuming deductibility. The rules have changed before and may change again.

HELOC Pros and Cons

Advantages

Flexibility. You borrow only what you need, when you need it. If your renovation comes in under budget, you don’t pay interest on money you didn’t use.

Lower initial payments. Interest-only draw payments are significantly lower than what you’d pay on a personal loan or home equity loan for the same amount.

Revolving credit. As you repay principal, your available credit replenishes. You can borrow, repay, and borrow again during the draw period.

Potentially tax-deductible. For qualifying uses, the interest deduction reduces your net borrowing cost.

Lower rates than unsecured debt. A HELOC at 8.75% is much cheaper than a personal loan at 14–18% or a credit card at 22%+.

Disadvantages

Variable rate. Your payment can increase if rates rise. Two rate hikes of 0.25% each add $42/month to a $100,000 HELOC.

Your home is collateral. Miss enough payments and you can lose your house. This is not a loan to take casually.

Payment shock. The jump from draw to repayment catches people off guard. Use the calculator to see your repayment payment before you sign.

Closing costs. Most lenders charge 2–5% of the credit limit in fees. Some offer no-closing-cost HELOCs, but those usually come with higher rates.

Temptation to overborrow. Revolving access to a large credit line can lead to using more than planned.

How to Get a HELOC: Step by Step

Step 1: Check your equity. Use the calculator above to estimate your maximum available credit line. You need at least 15–20% equity in your home after the HELOC.

Step 2: Check your credit score. Pull your credit report before applying. Scores below 680 will limit your options. Above 740 gives you the best rates.

Step 3: Calculate your DTI. Add up all monthly debt payments (mortgage, car, student loans, minimum credit card payments) and divide by gross monthly income. Most lenders want this below 43%.

Step 4: Shop at least 3 lenders. Check your current bank, a credit union, and at least one online lender. Rates and fees vary more than you’d think.

Step 5: Gather documents. Lenders typically want: recent pay stubs, two years of tax returns, recent mortgage statement, proof of homeowners insurance, and a government-issued ID.

Step 6: Get an appraisal. Most lenders will order an appraisal to confirm your home’s value. Some use automated valuations for smaller HELOCs.

Step 7: Review the terms carefully. Check the margin above prime, the rate cap (maximum rate you can ever be charged), any annual fees, and early closure penalties before signing.

HELOC Payment Examples

These examples use an 8.75% interest rate and a 10-year draw / 20-year repayment structure.

HELOC Amount | Draw Payment (Interest Only) | Repayment Payment |

|---|---|---|

$25,000 | $182/mo | $221/mo |

$50,000 | $365/mo | $442/mo |

$75,000 | $547/mo | $663/mo |

$100,000 | $729/mo | $884/mo |

$150,000 | $1,094/mo | $1,326/mo |

$200,000 | $1,458/mo | $1,768/mo |

Use the calculator above to run your exact numbers with your actual rate, draw period, and repayment term.

HELOC by State: What You Should Know

HELOC availability and rules vary by state. A few things to be aware of:

Texas has historically had strict home equity lending rules. You can borrow up to 80% CLTV, but there are restrictions on the number of home equity loans you can have and specific waiting periods after closing.

California borrowers can access up to 85% CLTV at some lenders and benefit from one of the most competitive HELOC markets in the country given high home values.

Florida has homestead exemption laws that can complicate HELOC approval on primary residences. Work with a lender who knows Florida real estate law.

New York HELOC closings require an attorney in some cases, adding to closing costs and timelines.

State income tax also affects your after-tax cost. In states with no income tax (Texas, Florida, Washington, Nevada), you don’t get a state-level deduction. In high-tax states like California and New York, the federal deduction can be more valuable.

Frequently Asked Questions

Using This HELOC Calculator

The calculator at the top of this page covers every scenario you’re likely to encounter:

Draw period payment — see your interest-only minimum payment during the borrowing phase.

Repayment period payment — see the full principal-plus-interest payment after the draw period ends.

LTV check — enter your home value and mortgage balance and the calculator tells you the maximum HELOC you qualify for at 80%, 85%, or 90% combined LTV.

Rate scenarios — model your payments at your current rate, +1%, and +2% to stress-test affordability.

Extra payments — add an optional extra monthly payment to see how much faster you’d pay off the balance and how much interest you’d save.

Amortization schedule — the full month-by-month table showing interest, principal, and remaining balance for every payment from draw period to payoff.

All calculations use standard financial formulas. No account needed. Nothing is saved or stored.

This calculator is for informational purposes only and does not constitute financial advice. HELOC rates are variable and will change over time. Consult a licensed mortgage professional before making borrowing decisions. Tax deductibility depends on individual circumstances — speak with a qualified tax advisor.